"How do you afford to travel all the time?"

Tue Oct 16, 2018 · 8 min read

I live nomadically, which is a concise way of saying that I travel all the time and have no home base. Some call this being a “digital nomad,” but I don’t think that’s a descriptive term. Successfully travelling the world without blowing through cash has nothing necessarily to do with your career choice or skill set. It does, however, require some planning and intentional goals.

I’m frequently asked, “How do you afford to travel all the time?” This question is based on many misconceptions that I’ll do my best to set straight in this post.

Explaining how I afford to travel constantly first requires a little insight into one of my reasons for living the way I do in the first place.

I don’t tend to spend a lot by default. In comparison to most Canadians, the majority of which are still in growing debt, I have financial freedom. Maintaining a debt-free status understandably requires some level of discipline. Perhaps counter-intuitively, constant travel while living out of one bag actually aids me in maintaining discipline when it comes to spending.

Since I don’t have a house/car/large suitcase(s) with which to store or transport things I buy, I’m intentionally limiting myself to only acquiring items that can fit in the bag I carry on my back. This means that practices like impulse shopping are, a great majority of the time, countered by the knowledge that I simply don’t have the room to keep the things I might feel compelled to buy. Unlike going on vacation - a time during which many people I know will shop for days on end and sometimes even purchase extra luggage to take home their goods - my style of travel doesn’t allow for this flavour of frivolity.

There’s still plenty of intangible things in the world for me to spend money on, and I’m by no means a saint when it comes to avoiding unnecessary purchases. Usually, however, I successfully avoid traps like impulse spending. My general philosophy regarding money is a large part of that success.

I tend to view money a little differently, I think, than most people, and certainly differently than I did even five or ten years ago. Rather than thinking of “spending money” or “saving money,” the best way I can describe my perspective is that I think of money as a general resource. Largely, its presence is a byproduct of how I spend my time.

Here’s an overview of the key points in how I tend to think about money.

Instead of thinking of dollars as numbers attached to some theoretical bank account, I consider my money to be largely equivalent to my time. In other words, it’s helpful to put a monetary value on your own time. Doing so puts some common time sinks in perspective.

If you currently have work that earns you money, it can make sense to outsource errands that have a high time cost - like by utilizing food delivery, cleaning, and childcare services. For example, if paying $10 to have food delivered saves you two hours of fetching groceries and cooking, and you can currently earn $15 an hour, then paying for food delivery will make you $20 ($15 x 2 hours = $30, $30 - $10 = $20), assuming you use the time you save to earn money.

As a counter example, I’ve visited some countries where wash-and-fold laundry services are priced by the weight of the clothing in kilograms. In some cases, it was as much as $10/kg. If you had 9kg of clothing to wash (a typical laundromat load for some) it would have cost $90. In this case, if you earn $15 an hour, it’s monetarily to your advantage to wash your own clothing, assuming you can do so in less than 6 hours ($90 divided by $15 = 6).

At the very least, it’s a worthwhile exercise to do the math and assess where you might be leaking your earning potential.

Given the decision to purchase an expensive, high-quality item or an inexpensive, lower-quality item, I will almost always choose the former. This pertains especially to goods that get a lot of use, like clothing, electronic equipment, and bags. Besides the obvious appeal of having a higher-quality item in the immediate term, high quality is (not always, but usually) indicative of durability. The benefit of durable goods is that you need to replace them less often.

Here’s an illustrative, real-life example. My carefully chosen clothing includes some racerback tank tops made by Lululemon, a notoriously pricey brand. Not everything the company makes is of good quality, but I’ve found these particular tops to be very well made - as evidenced by the fact that they’ve been in constant (weekly) use for the last two years, and they still look new. In direct contrast, there is the infrequent occasion of my forgetting this particular point of my philosophy and buying a cute and inexpensive clothing item. None of those rash purchases have resulted in a piece of clothing that didn’t fray, wear, or in the case of one sweater, unravel in under a month.

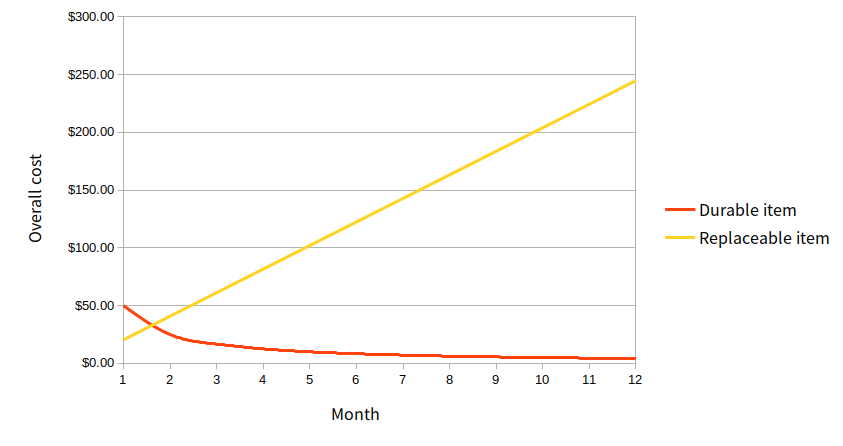

This point is best illustrated by thinking in terms of the average monthly cost of goods - the amount of money you’d pay in a month to purchase and/or replace something. In the case of the Lululemon top, I paid roughly $50 for an item that has so far lasted two years. We can consider its average monthly cost to be (so far) about $2.08 ($50 divided by 24 months). In the alternate case, I paid roughly $12 for a top that came undone at the seams after two weeks. Its average monthly cost? About $20.

A very scientific chart showing the total cost of a durable item vs. a replaced item over the span of a year.

If I expect to make use of something for a good long time - both due to its durability and my own desire to use it - I’ll almost always opt to spend more money on it now, rather than choose an cheaper alternative. In the long run, the latter is too expensive.

Another aspect to planning to have money in the future is deciding what you intend to do with it. This covers a few more dimensions than you might immediately think - for me, it ties in to everything from travel plans to the colour of my clothing.

When I make important purchase decisions, I typically think two or three purchases ahead. In the case of travel plans, this might translate to choosing a flight route with stopovers that get me incrementally closer to an ultimate destination. This way, instead of taking long and expensive flights that retrace miles, I plan to take shorter, usually cheaper flights that keep me moving towards a final location, usually over a period of weeks or months if my schedule allows. I can then use those stopovers to add overall value to my trip - either by taking business meetings, seeing friends, or visiting new places.

I similarly plan ahead when I purchase physical goods. In the particular case of my wardrobe, the single greatest decision I made to simplify future clothing purchases was to build a capsule wardrobe with only black clothing. When I need to replace or purchase a new item, I never worry that colours or patterns won’t match. I also haven’t yet come across anything I’ve needed that wasn’t available in black. This one change has all but eliminated decision fatigue for me when it comes to clothing.

I also chose black because I think it covers the greatest possible range of dress codes and social situations for which a single colour can be appropriate. If all-black sounds a little too restrictive for you, I’d suggest building a wardrobe in the smallest range of colour shades that appeals to you - for example, all shades of blue, or to go slightly broader, blue-greens.

Ultimately, the fundamental concept in planning future purchases is to not create an outlier, if you can avoid it. Don’t buy a piece of tech that requires its own unique charging port and cable, for instance, if you can get something similar that uses the same USB-C charger as the rest of your electronics.

As well as striving to optimize my money over time, I also try and get the most value that I can from my spending. Simply, this means spending money on things that I actually care about, and that bring me joy.

I avoid nights of going drinking, because buying alcohol at bars is an expensive way to misplace your mental faculties. I avoid impulse shopping for things I can’t carry, and I don’t subscribe to product mailing lists. I don’t upgrade all my electronics each year. I’m fine with cheap meat and cheap coffee, most days.

What do I buy? Mostly, time and experiences. If it’s worth my while to afford it, I pay for great service, amazing views, or to put myself in the company of competent people who are experts in their field. I care about seeing new places, trying amazing food, and having experiences that shake up my perspectives. These are things that make me feel wealthy, successful, and happy.

Teatime with a view at the Peak Lounge at Park Hyatt Hotel, Tokyo.

Hopefully, I’ve demonstrated that there’s no special magic to how I afford to travel constantly. Living this way isn’t, like some folks think, being on permanent vacation - I still strive to be smart and responsible when it comes to earning and spending.

Putting a physical limit - one bag - on being able to amass things is helpful when it comes to keeping the stuff I own in perspective. Beyond that, my spending habits don’t look very different from someone who might live in a single location - except that my transportation costs may tend more towards plane rides than vehicle payments, and I generally purchase experiences over “stuff.”